(Image via

(Image viaManaging finances as the end of the month approaches can often feel overwhelming. Many people find themselves worried about bills, unclear about their remaining funds, or unsure how to allocate resources effectively. These challenges can lead to stress and prevent you from enjoying your hard-earned money. However, with simple tactics and a clearer structure, the pressure of end-of-month finances can be reduced significantly.

This guide will help you understand practical steps to manage cash flow, build financial stability, and ease the strain of budgeting when closing a month’s finances. By following these methods, you’ll gain more control over your money, reduce stress, and set the foundation for better financial habits moving forward.

Understand the Common End-of-Month Challenges

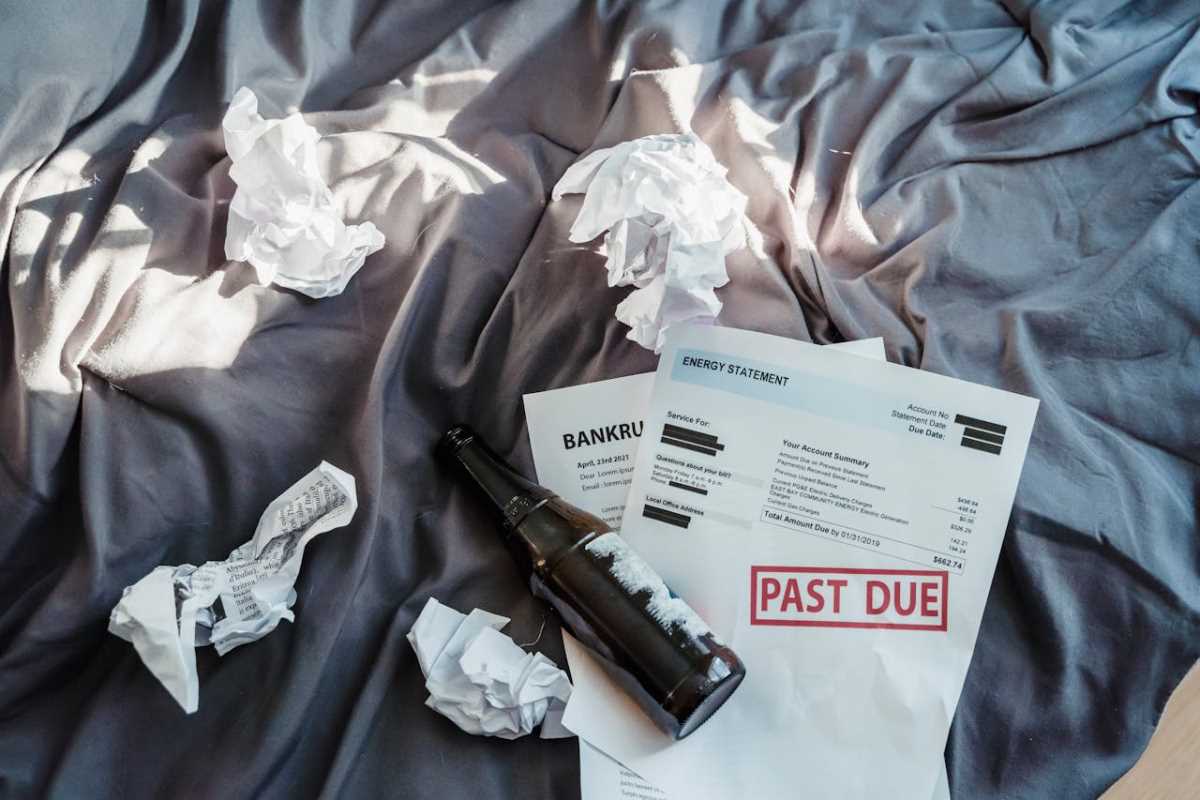

End-of-month stress often stems from poor planning, unexpected expenses, or a lack of visibility into finances. A common issue is running out of money before the next paycheck arrives, leaving little room for unplanned costs. For instance, unexpected utility bill increases or last-minute grocery needs can quickly derail plans if no safety net is in place.

Other challenges include juggling multiple payment deadlines, struggling to track spending within your budget, or discovering that certain financial goals—like savings—have been neglected throughout the month. These small, yet frequent, roadblocks can snowball, creating anxiety about how to meet basic needs.

Take Control with Smart Techniques

Reducing financial stress requires preparation, structure, and a focus on long-term solutions. Below are effective strategies that can reshape how you approach and manage your end-of-month finances.

1. Budget Proactively at the Start of the Month

Setting a budget early on is critical for avoiding last-minute scrambling. Allocate your income across categories like essentials, savings, debt repayment, and discretionary spending. A popular approach is the 50/30/20 budgeting rule—50% of income goes toward needs, 30% toward wants, and 20% toward savings or paying debts.

Breaking expenses into categories ensures that every dollar has a purpose. Consider non-monthly costs like annual subscriptions or seasonal expenses, and divide their total over each month of the year to better prepare. Writing down or digitally tracking these projections provides a clear overview, minimizing surprises later.

2. Prioritize Fixed Costs and Necessities

Fixed costs such as rent, utilities, transportation, and minimum debt payments shouldn’t be left to chance. Dedicate a portion of your paycheck to these essentials as soon as it hits your account. Automating payments is an excellent way to prevent late fees and ensures these critical costs are covered without constant oversight.

By addressing these expenses first, you’ll gain peace of mind knowing your primary needs are secured before moving on to discretionary spending.

3. Track Spending Weekly

Checking in with your budget weekly instead of waiting until the end of the month can avoid unnecessary stress. Think of these check-ins as a financial status update—review all recent expenses and compare them to your allocated budget.

Spending usually increases toward the end of the month, especially with impulse purchases or overlooked costs like gas or groceries. Tracking regularly establishes accountability and creates opportunities to make small course corrections before overspending happens.

Budgeting apps like Mint, YNAB (You Need A Budget), or even a simple spreadsheet can help you consistently monitor cash flow.

4. Build a Financial Cushion

An emergency fund prevents unexpected expenses from derailing your finances. Setting aside even a small percentage of your income into a savings account builds a buffer over time. This safety net can be used for anything—car repairs, medical bills, or even an urgent need for groceries—without tapping into funds for rent or other essentials.

To make saving easier, start by automating transfers into a separate savings account each payday. Small contributions, like $10 or $20 per paycheck, can add up faster than expected and reduce financial stress as sudden costs arise.

5. Manage Variable Expenses Wisely

Variable expenses, like groceries, dining out, and entertainment, are often where most people overspend. Adjust these amounts as needed to accommodate tight months without undermining your fixed and essential costs.

For example, compare prices and shop strategically when grocery shopping. Planning meals ahead of time not only reduces food waste but also prevents overspending. Similarly, find free or low-cost activities to replace more expensive outings.

Cash budgeting techniques, such as the envelope system, can keep variable spending under control. For each category, withdraw cash equal to the amount budgeted, and place it in a labeled envelope. Spend only the cash allocated for that purpose, which limits the risk of exceeding your budget.

6. Bring Clarity to Payment Deadlines

Late bills amplify the financial strain of end-of-month budgeting. Avoid disruptions by creating a visual payment schedule. Mark due dates on a calendar, whether paper or digital, and set reminders a few days before each deadline.

Consolidating some payments, like utilities or credit cards, to the same date each month reduces the number of deadlines to track. Speak with service providers if adjusting dates helps you stay in control of your finances.

7. Resist the Urge to Use Credit

It’s tempting to rely on credit cards during tight periods, but this can easily spiral into long-term debt. Treat credit as a last resort. Instead, revisit your budget and find areas to scale back spending for the current month.

For essentials requiring credit purchases, plan to pay them off as quickly as possible to minimize interest charges. Reducing impulsive credit usage helps you stay focused on financial goals without incurring unnecessary additional costs.

8. Review Your Financial Success Each Month

Reflection helps improve your approach to finances. At the end of every month, take five to ten minutes to review how well you adhered to your budget. Were there specific areas where you spent more than planned? Did an unexpected expense catch you off guard?

Use this time to adjust future budgets and refine your strategy. Improvements, no matter how small, positively impact your long-term financial health.

Easy Fixes for Common Obstacles

Tight months don’t mean you’re stuck without options. Here are actionable fixes for frequent problems:

- Unmanaged Expenses: Use a budgeting app or switch from digital tracking to written lists if visibility feels unclear.

- Too Many Impulses: Install a 24-hour “wait rule” for non-essential purchases—this ensures you only commit to expenses aligning with your goals.

- Missed Payments: Add automated scheduling for consistent bills, reducing the risk of forgetting important deadlines.

Set yourself up for long-term success by creating habits that reduce stress and improve your overall financial well-being. Take those first steps today, and soon, end-of-month finances will feel manageable and rewarding instead of overwhelming.